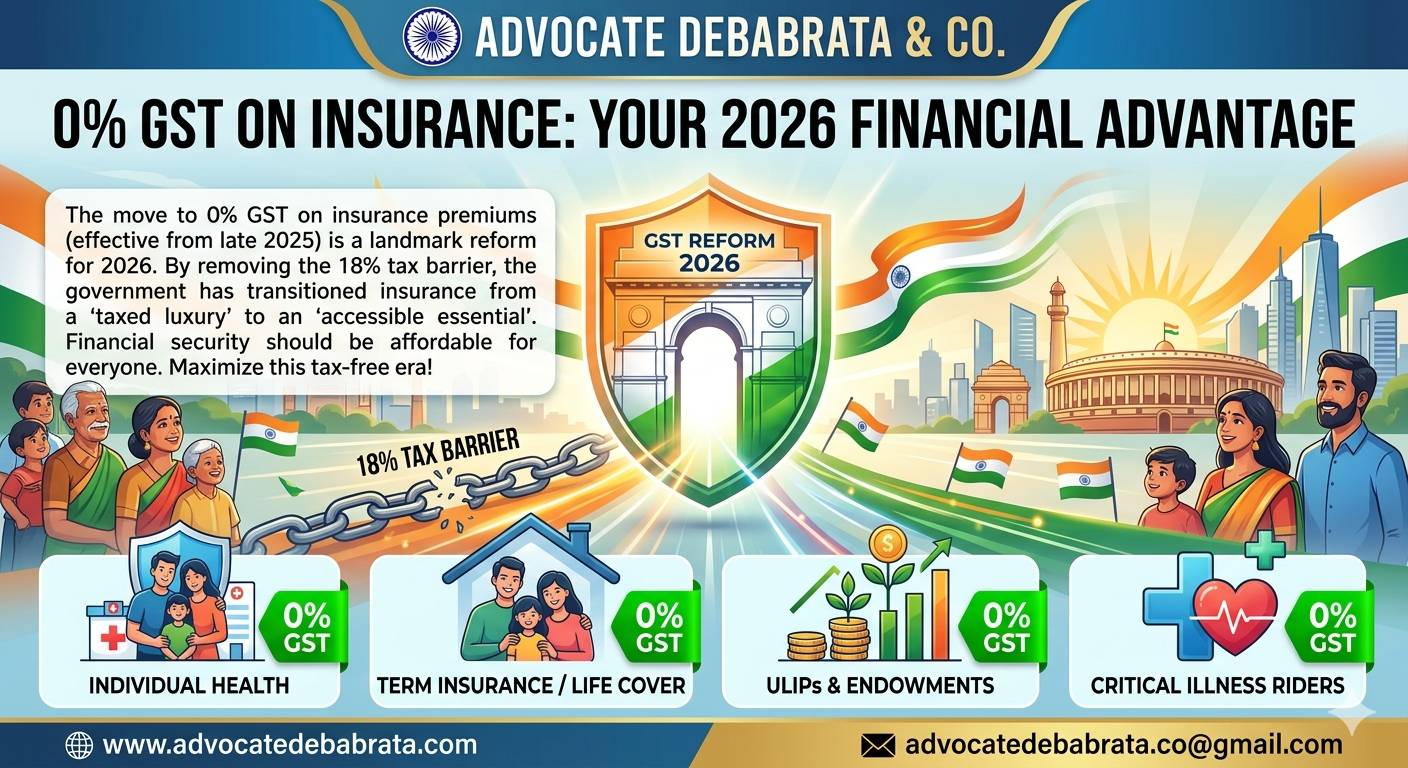

One of the biggest financial wins of recent times is the removal of the 18% GST on insurance premiums, which came into effect in late 2025. For years, insurance was treated like a luxury and taxed accordingly. That’s finally changed — it’s now treated as the essential necessity it always should have been.

At Advocate Debabrata & Co., we’ve always believed that financial protection shouldn’t come with a tax penalty. So here’s a plain-English breakdown of what this means for you.

The Simple Math

Before this change, if your health or life insurance premium was ₹20,000, you were actually paying ₹23,600 — the extra ₹3,600 went straight to the government as GST. Now? You pay exactly what the policy costs. Nothing extra.

This applies to individual health insurance, term life, ULIPs, endowment plans, and even riders like critical illness cover. The one exception is corporate group insurance, which still carries the 18% GST.

Three Smart Ways to Use the Savings

- Get more cover for the same money Instead of spending less, you could keep your budget the same and simply buy a plan with better coverage — a higher sum insured, wider hospital network, or stronger add-ons.

- Let your investments grow faster In ULIPs and endowment plans, part of your premium used to get eaten up by GST on service charges. Over a 20-year plan, that could quietly drain ₹18,000 or more from your investment corpus. That money now stays invested and compounds in your favour.

3. Real relief for senior citizens A ₹50,000 health policy for a senior used to come with a ₹9,000 tax burden on top. For someone on a fixed pension, that’s a significant hit. That burden is now completely gone.

What’s Tax-Free and What Isn’t?

Type of Insurance | GST Now |

Individual health insurance | 0% |

Term life insurance | 0% |

ULIPs & endowment plans | 0% |

Critical illness riders | 0% |

Corporate/group cover | 18% (unchanged)

|

Common Questions

Will my premium automatically go down? Yes — you’ll see the difference at your next renewal. No action needed on your part.

Do I need to buy a new policy? No. Insurers have already updated their systems.

Should I wait before buying? Definitely not. Premiums rise with age, so buying sooner locks in a lower base rate — and the 0% GST benefit is already live.

A Few Tips Before You Buy

Don’t just hunt for the cheapest premium. Use the savings you’re making to actually strengthen your coverage — add a critical illness rider, choose insurers with strong claim settlement records, and look for cashless hospital networks that work for you.

For guidance on making the most of India’s changing tax landscape — whether personal or business — reach out to Advocate Debabrata & Co.

🌐 www.advocatedebabrata.com 📧 advocatedebabrata.co@gmail.com