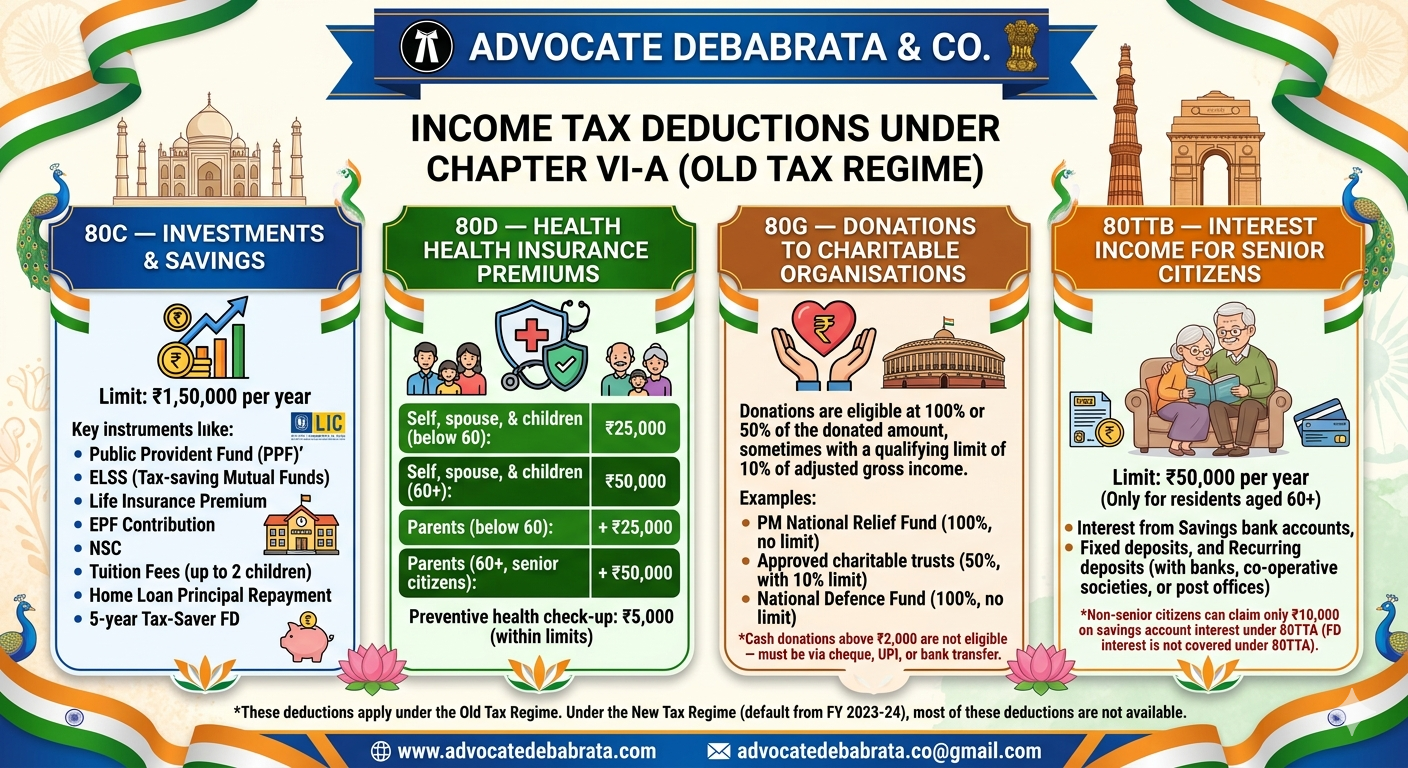

Income Tax Deductions Under Chapter VI-A

These deductions reduce your taxable income, thereby lowering your tax liability.

80C — Investments & Savings

Limit: ₹1,50,000 per year

The most popular deduction, covering a wide range of investments and expenses:

| Instrument | Example |

|---|---|

| PPF | Depositing ₹50,000 in Public Provident Fund |

| ELSS | Investing ₹30,000 in a tax-saving mutual fund |

| Life Insurance Premium | Paying ₹20,000 annual premium for an LIC policy |

| EPF | Employee’s share of provident fund contribution |

| NSC | Buying National Savings Certificates |

| Tuition Fees | Paying school fees for up to 2 children |

| Home Loan Principal | Repaying the principal portion of a housing loan |

| 5-year Tax-Saver FD | Locking ₹1.5L in a bank tax-saving FD |

Example: Ravi invests ₹70,000 in PPF, pays ₹40,000 as LIC premium, and ₹40,000 in ELSS. Total = ₹1,50,000 → full deduction claimed.

80D — Health Insurance Premiums

Limit: Varies by age

| Who is covered | Limit |

|---|---|

| Self, spouse & children (below 60) | ₹25,000 |

| Self, spouse & children (60+) | ₹50,000 |

| Parents (below 60) | + ₹25,000 |

| Parents (60+, senior citizens) | + ₹50,000 |

| Preventive health check-up | ₹5,000 (within above limits) |

Example: Priya (age 35) pays ₹18,000 premium for her family’s health insurance and ₹32,000 for her senior citizen mother’s policy. She can claim ₹18,000 + ₹32,000 = ₹50,000 deduction.

80G — Donations to Charitable Organisations

Limit: Depends on the fund/institution

Donations are eligible at 100% or 50% of the donated amount, sometimes with a qualifying limit of 10% of adjusted gross income.

| Category | Deduction | Example |

|---|---|---|

| PM National Relief Fund | 100%, no limit | Donating ₹10,000 → ₹10,000 deduction |

| Approved charitable trusts | 50%, with 10% limit | Donating ₹20,000 → ₹10,000 deduction |

| National Defence Fund | 100%, no limit | Full amount deductible |

Example: Arjun has a gross income of ₹8,00,000. He donates ₹60,000 to an approved charity (50% with limit). The qualifying limit is 10% of adjusted income = ₹80,000. So 50% of ₹60,000 = ₹30,000 is deductible.

Cash donations above ₹2,000 are not eligible — must be via cheque, UPI, or bank transfer.

80TTB — Interest Income for Senior Citizens

Limit: ₹50,000 per year (Only for residents aged 60+)

Covers interest from:

- Savings bank accounts

- Fixed deposits

- Recurring deposits (with banks, co-operative societies, or post offices)

Example: Meena (age 67) earns ₹35,000 interest from her SBI FD and ₹10,000 from her savings account. Total interest = ₹45,000 → entire ₹45,000 is deductible under 80TTB.

Non-senior citizens can claim only ₹10,000 on savings account interest under 80TTA (FD interest is not covered under 80TTA).

Quick Comparison Summary

| Section | Who | Max Deduction | What |

|---|---|---|---|

| 80C | All individuals | ₹1,50,000 | Investments, insurance, tuition |

| 80D | All individuals | ₹25,000–₹1,00,000 | Health insurance premiums |

| 80G | All taxpayers | 100%/50% of donation | Charitable donations |

| 80TTB | Senior citizens (60+) | ₹50,000 | Interest from deposits |

Note: These deductions apply under the Old Tax Regime. Under the New Tax Regime (default from FY 2023-24), most of these deductions are not available.