INPUT TAX CREDIT

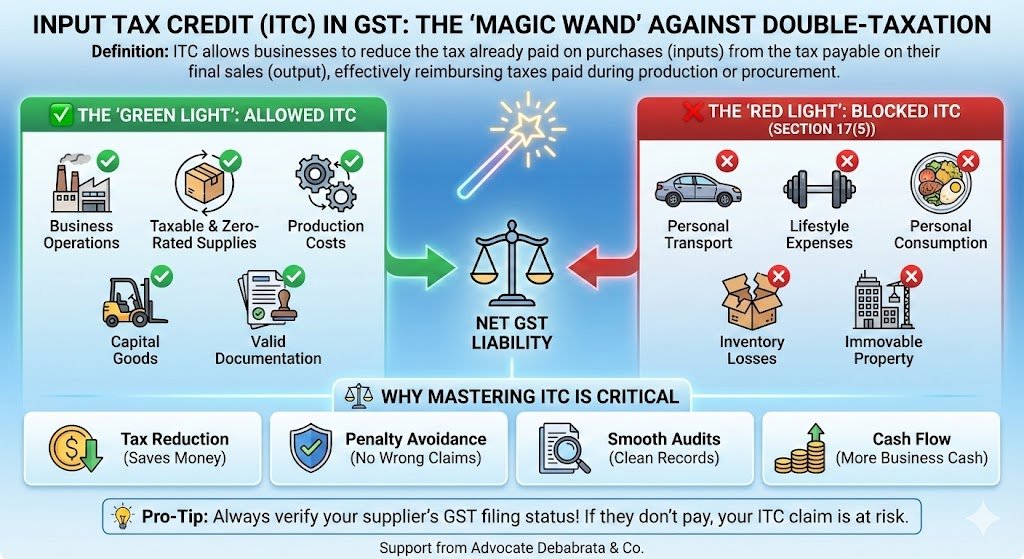

The world of Goods and Services Tax (GST) can feel like a labyrinth, but Input Tax Credit (ITC) is the thread that leads you out. ITC is the mechanism where a business can reduce the tax it has already paid on inputs (purchases) from the tax it is liable to pay on its output (sales).

Without ITC, we would suffer from the “cascading effect,” or tax-on-tax, which inflates costs for everyone. Here is an expanded, deep-dive guide into the mechanics of ITC, specifically focusing on the “Blocked Credits” under Section 17(5).

The Mechanism of ITC

At its core, ITC ensures that GST is a tax only on the value addition at each stage of the supply chain.

The Golden Formula:

Net GST Liability = Total Output Tax – Total Eligible ITC

Prerequisites for Claiming ITC (Section 16)

Before looking at what is blocked, you must meet these four criteria:

- Possession of Invoice: You must have a valid tax invoice or debit note.

- Receipt of Goods/Services: The items must have actually been delivered.

- Tax Paid to Government: Your supplier must have actually deposited the tax collected from you.

- Return Filed: You must have filed your GSTR-3B.

The “Green Light”: Where ITC Flows Freely

Most business-related expenses are eligible. Here are specific examples to help you identify them:

- Raw Materials & Consumables: Steel for a car manufacturer, flour for a bakery, or ink for a printer.

- Professional Fees: GST paid on services from legal consultants (like Advocate Debabrata & Co.), auditors, or marketing agencies.

- Capital Goods: If a textile mill buys a power loom for ₹10 Lakhs + 18% GST, that ₹1.8 Lakh can be used to offset output tax.

- Utility & Services: Business internet bills, cloud hosting services (AWS/Azure), and office rent.

The “Red Light”: Blocked Credit (Section 17(5))

Section 17(5) is the “Negative List.” Even if these expenses are for your business, the government says “No” to the credit.

|

Category |

The General Rule (Blocked) |

The Exception (Allowed) |

|

Motor Vehicles |

For transport of persons with seating capacity $\le 13$. |

Used for: Further supply (dealers), Transportation of passengers, or Driving schools. |

|

Food & Catering |

Food, beverages, outdoor catering, cosmetic/plastic surgery. |

If it is obligatory for an employer to provide these under any law (e.g., Factory Act). |

|

Lifestyle/Social |

Membership of clubs, health centers, and fitness centers. |

No exceptions generally apply here. |

|

Construction |

Goods/services for construction of “Immovable Property” (on own account). |

Construction of Plant & Machinery is fully eligible for ITC. |

|

Lost/Gifted Goods |

Goods lost, stolen, destroyed, or given as free samples. |

None. You must “reverse” the ITC if already taken. |

Critical Case Laws to Know

Legal precedents often clarify the “gray areas” of the law.

- Safari Retreats Pvt. Ltd. vs. Chief Commissioner (Odisha High Court):

The petitioner built a shopping mall to let out. The court held that if the intent is to provide taxable services (renting), the ITC on construction materials should not be blocked, as it defeats the purpose of GST. Note: This is currently under challenge in the Supreme Court.

- M/s. Wipro Limited (AAAR Karnataka):

Clarified that ITC on “Group Insurance” for employees is only available if such insurance is mandated by the government during specific periods (like COVID-19 mandates or the ESI Act).

Why Strategic ITC Management is Vital

- Cash Flow Optimization: Using ITC effectively means less “real cash” leaves your bank account during monthly filings.

- Pricing Competitiveness: If you can’t claim ITC, that tax becomes a cost. This forces you to increase your product price, making you less competitive.

- Audit Protection: Claiming blocked credit is a major red flag for the GST department. Proper categorization prevents expensive litigation later.

Pro-Tip: The “2B” reconciliation is your best friend. Always ensure your GSTR-2B matches your purchase register. If your supplier is a “tax-evader,” you lose your credit!

How can we help?

Navigating the nuances of Section 17(5) requires a keen legal eye to ensure you aren’t leaving money on the table—or accidentally inviting a tax notice.

Would you like me to draft a sample reconciliation sheet to help you track your eligible vs. ineligible ITC for this month? Or perhaps you’d like more details on the Safari Retreats case? Under the guidance of Advocate Debabrata & Co., we can ensure your compliance is airtight.